Can ‘Build-to-Rent’ finally flourish in the UK?

By lucmin on 25th September 2017

For over a decade, institutional investors have been on the verge of ‘breaking the UK market’ for residential rental provision. Progress has been hampered by some significant challenges including planning, access to finance, providing returns, competing for land and the mind-set of UK households who view renting as secondary to owning your own home. But now it seems that a combination of policy changes and a weaker sales marker may have created the right conditions for institutional investment to finally flourish in the UK.

Since the UK has virtually no existing stock of rental homes available for bulk investors to build a portfolio, Build to Rent (BTR) has become the preferred route to market, whereby investors will create their own purpose-built stock.

It is widely assumed that the demand for renting from a professional landlord will largely derive from ‘Generation Rent’. The term Generation Rent emerged to describe a new type of renter – younger professional singles and couples primarily located in London and other large regional cities who choose to rent for longer. This segment of the population turned to rental market in the years since the financial crisis, when stricter mortgage regulations and rising stamp duty contributed to a less active housing market and rates of new housing delivery continually failed to meet demand.

Some of these ‘lifestyle renters’ will pay a premium for specification, amenities and location and this, combined with their prospects for career progression and rising disposable income, makes them attractive to investors. Unsurprising then that attention has been focussed on this segment of the market with providers looking for ways to deliver a top-end product and maximise their returns. But more research is required to explore the levels of demand that may be present in other household types and in different locations. The potential returns available in the mainstream rental market may have been overlooked.

Looking ahead, it has been suggested that the BTR sector could be affected by the uncertainty of Brexit as a fall in the number of EU citizens taking up employment in UK cities could reduce demand for rental homes. However, the case for investment is gaining traction and a recent House of Commons briefing paper drew attention to its defensive qualities making it attractive when compared to commercial investment over the longer term:

“Residential’s low correlation with commercial property is likely to serve it well. The sector proved its defensive characteristics during the steep market downturns in both the 1990s and 2000s, when residential property not only recorded a smaller capital decline than its commercial counterpart but also recovered its initial value faster. Pension funds and other long-term institutional investors are very much aware of this”.

One recent example of institutions’ appetites for expanding their PRS portfolios, is Grainger’s purchase of a development site in Salford, Manchester for £80m on which to deliver 375 PRS units by 2020. Grainger is a co-investor of one of the UK’s largest market-let residential investment funds (REIT) GRIP.

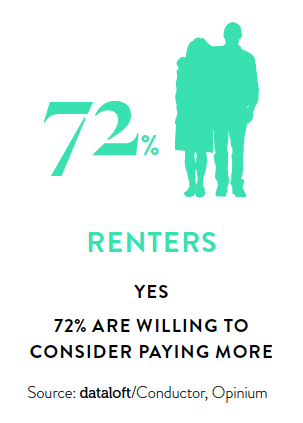

As the interest in BTR grows from all sides (developers, investors, potential tenants and the government), property firms seek to improve their understanding of this market place and position themselves as experts. This has resulted in a slew of surveys designed to explore tenant preferences and profiles with an arms race to bag the largest number of respondents. A recent study by Conductor and SAY, with support from Dataloft, showed that 72% of renters say they would be willing to consider paying an extra 10% in rent for a purpose-built apartment.

Would renters pay an extra 10% in rent for a purpose-built apartment?

The key, as ever, is in the way the questions are posed – it is no good finding out that 75% of tenants would like a swimming pool if they are not minded, or in a position, to pay a premium rent for it.

A survey earlier this year by Knight Frank shows that just 30% of those surveyed and living in the PRS still have their eye on being able to own their home one day and are renting while they save for a sufficient deposit. It would be interesting to know if this is the attitude of a particular group within the sample, perhaps defined by age, life-stage, income, household size and/or location. Interestingly, 21% of the tenants surveyed stated that living in the PRS enables them to live in an area where they would not be able to afford to buy a home.

This kind of research flags up the challenges of asking for opinions on a product that is still a rarity, from a group of people who, in the main, had not experienced the lifestyle being proposed.

There is certainly scope for further research to better understand how this market is evolving, including monitoring whether public perceptions towards BTR are changing. In addition to winning over the general public to consider long-term renting from a professional landlord, PRS providers also face the challenges of obtaining planning permission for build to rent schemes and proving returns for their investors.